Introduction

The shift toward a net-zero world is reshaping global markets, regulations, and corporate expectations. Countries are enacting stricter carbon laws, while investors and consumers demand low-carbon leadership.

For businesses, this creates transition risks: challenges and costs organisations face as economies shift to low-carbon models. These risks stem from regulatory changes, market transformations, technological shifts, and reputational or litigation pressures associated with the decarbonization process. Unlike physical risks (e.g., floods or wildfires), transition risks are strategic, financial, and operational in nature, and they are increasingly urgent.

Categories of Transition Risks

Transition risks are dynamic and interconnected. They can be broadly categorized into four key areas by leading standards, such as the TCFD and CSRD.

- Policy & Legal Risks

New laws and regulations, such as carbon taxes, emission caps, mandatory climate disclosures, or sector-specific mandates, can impose direct financial burdens on companies. Also, litigation risks are rising as more lawsuits are being filed against firms for failing to adapt or disclose climate-related risks. For instance, the EU’s Carbon Border Adjustment Mechanism (CBAM) imposes a carbon tax on certain imports, creating a direct financial risk for companies that rely on high-carbon supply chains.

- Technology Risks

As cleaner technologies emerge (e.g., renewables, green hydrogen, carbon capture), older assets can become stranded. Businesses that fail to invest in low-carbon technologies risk being outpaced by more innovative competitors. A report from Carbon Tracker estimated that $2.4 trillion in oil and gas projects could become stranded assets by 2035 due to declining demand and competition from renewable energy sources. (Carbon Tracker)

- Market Risks

Consumer demand is shifting toward sustainable products. Input costs may rise (e.g., for low-carbon materials). Firms that lag may lose market share. For example, some studies cite that 69% of global consumers have changed their purchasing behaviour due to climate concerns. (Statista)

Additionally, investor pressure is a powerful market force; according to research from EY, 70% of global investors surveyed say they are likely to divest from companies with poor ESG performance. This pressure influences everything from a company’s access to capital to its stock valuation. (EY)

- Reputation Risks

In the age of social media and stakeholder activism, a company’s climate stance is under constant scrutiny. Misleading environmental claims, also known as “greenwashing,” can result in severe reputational damage and a loss of brand trust. Conversely, transparent and credible climate action can significantly enhance brand value, strengthen customer loyalty, and attract top talent.

Business Implications: From Risk to Reality

The implications of these risks are tangible and can directly impact a company’s bottom line:

- Stranded Assets: As the world shifts away from fossil fuels, “stranded assets” facilities, reserves, and capital rendered obsolete are projected to cost up to $8 trillion globally. For example, coal power stations and oil reserves lose value when regulation and clean alternatives limit demand.

- Increased Costs: Companies must invest heavily in tracking, reporting, and reducing emissions. Many firms are hiring new compliance staff and updating systems to meet evolving mandates.

- Competitive Disadvantage: Early movers who invest in cleaner technology and processes can gain a first-mover advantage, capturing new markets and improving efficiency while laggards are left to catch up.

- Financial Exposure: As climate risk becomes a core part of economic analysis, companies with poor transition plans may face a higher cost of capital. They may also be excluded from “green” or sustainable investment funds, limiting access to a growing pool of capital.

- Business Model Disruption: Sectors such as automotive and energy are undergoing significant reinvention. The swift move to EVs is disrupting both manufacturers and supply chains; those slow to adapt risk obsolescence.

Sector-Specific Vulnerabilities

Specific sectors face amplified transition risks:

- Oil, Gas, and Coal: High risk from regulations, market shifts, and reputational challenges.

- Automotive and Transportation: Accelerated EV timelines disrupt supply chains, exports, and traditional employment.

- Finance: Pressure to decarbonize lending and investment portfolios intensifies, leading to asset divestment or loss.

- Heavy Industry: Steel, cement, and chemicals confront costly shifts to new technologies or cleaner energy sources.

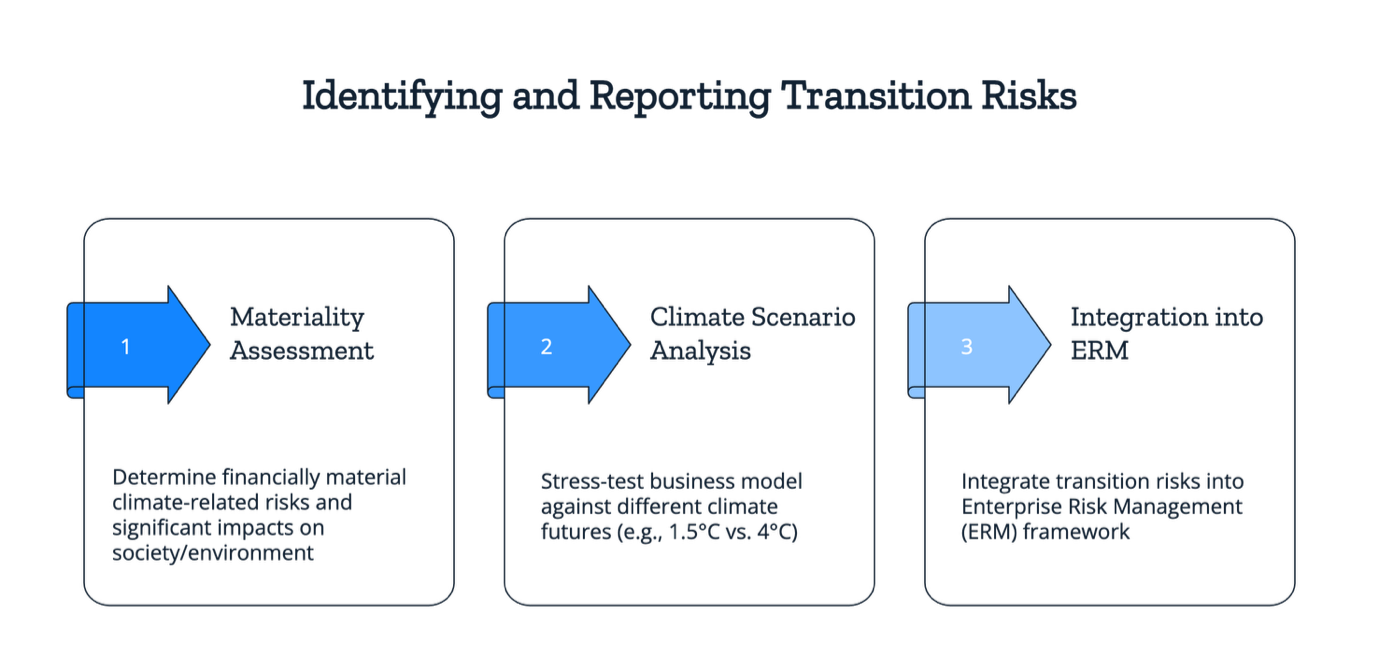

Identifying and Reporting Transition Risks

To manage these risks, companies must first identify them. This process involves:

- Materiality Assessment: Under frameworks such as the CSRD and ISSB, companies must conduct a double materiality assessment to determine which climate-related risks are most financially material to their business and which of their impacts are most significant to society and the environment.

- Climate Scenario Analysis: This involves stress-testing a company’s business model against different climate futures (e.g., a 1.5°C scenario vs. a 4°C scenario) to understand potential impacts and develop resilient strategies. A recent study across supply-chain networks found that at a CO₂ price of € 45/ton, firms may face direct sales losses of 1.3%, with cascading supply-chain effects multiplying the risk. (arXiv)

- Integration into ERM: Transition risks should not be siloed but integrated into the company’s broader Enterprise Risk Management (ERM) framework, ensuring the board and senior management regularly review them.

Strategies to Manage Transition Risks

Proactive companies are not simply reacting; they are using these risks as a catalyst for innovation and growth.

- Proactive Compliance Planning

Instead of waiting for new laws to take effect, companies should proactively build systems to collect and manage the data that will be required.

- Investment in Clean Technology & Innovation

A core strategy is to invest in R&D for low-carbon technologies, a process that can unlock significant cost savings and new revenue streams.

- Supplier Engagement & Value Chain Decarbonization

Partnering with suppliers to improve their own climate performance is crucial, as a significant portion of a company’s emissions often lies in its value chain. - Governance & Accountability

Spin up a climate or ESG committee with board oversight; assign executive-level accountability for transition execution.

Conclusion

Transition risks are a new reality for modern business. Transition risks are on par with physical climate risks in shaping a company’s long-term viability. While physical risks represent a clear and present danger, transition risks are shaping the future of business operations, finance, and competitive advantage

By treating these risks as a core strategic challenge, companies can build long-term resilience, attract green capital, and foster the trust needed to thrive in a low-carbon world. Whether by design or default, transition is inevitable; those who act today will shape tomorrow’s markets.

Future-proof your business against transition risks with Credibl’s AI-powered Climate Risk Platform. From scenario planning to audit-ready reporting, we help you manage risks, build resilience, and unlock competitive advantage.

Book a demo today and turn ESG transition risks into growth opportunities.

FAQ: Transition Risks in ESG

- What is a transition risk in ESG?

The financial, operational, and reputational risks businesses face as economies shift to low-carbon models. - How do transition risks differ from physical risks?

Physical risks are the direct impacts of climate change (e.g., floods), while transition risks arise from shifts in regulatory, technological, market, and reputational landscapes. - Why are regulators so focused on transition risks?

Because unmanaged risks threaten corporate stability and broader economic resilience, disclosure helps investors price risk and identify opportunities. - Are transition risks already affecting businesses today?

For example, companies with high exposure are already facing higher capital costs and valuation discounts. - What is a “stranded asset”?

Carbon-intensive assets that lose value prematurely, such as fossil fuel power plants, are affected by carbon pricing. - Can transition risk become an opportunity?

Companies leading in decarbonization can access capital, attract customers, and build long-term resilience.