Introduction

California has once again taken the lead in climate regulation — this time with Senate Bill 261, the Climate-Related Financial Risk Act. Signed into law alongside SB 253, this legislation represents the United States’ most ambitious step toward integrating climate risk into financial disclosures.

While SB 253 focuses on carbon emissions data, SB 261 zeroes in on the financial implications of climate change — physical and transitional risks that could materially affect an organisation’s revenue, assets, or operations.

In this guide, we unpack what SB 261 requires, who must comply, reporting timelines, and how businesses can prepare for this new era of climate risk accountability.

What Is SB 261?

SB 261 (the Climate-Related Financial Risk Act) requires large companies doing business in California to publish biennial reports describing how climate change may impact their financial health and what actions they’re taking to manage those risks.

In plain terms:

It forces companies to treat climate change as a financial risk — not just an environmental issue.

The law is modelled closely on the Task Force on Climate-Related Financial Disclosures (TCFD) and is designed to align with upcoming ISSB standards and the SEC’s proposed climate disclosure rules.

To learn more about mandatory climate-related disclosure, click here.

Who Must Comply?

SB 261 applies to public or private companies that:

- Do business in California,

- Have total annual revenues exceeding USD 500 million

Importantly, it does not require the company to be headquartered in California — meaning any business that operates, sells, or employs in the state may fall under its scope.

That makes this one of the broadest state-level disclosure mandates in U.S. history.

CARB is leading implementation and has issued guidance and workshops; it must adopt regulations for penalties and may issue further rules, with the first disclosures due by January 1, 2026, based on 2025 fiscal year data.

Exemption: Insurance companies regulated by a state Department of Insurance are not covered by SB 261. (LegiScan)

What Does SB 261 Require Companies to Report?

Each company in scope must prepare a “Climate-Related Financial Risk Report” at least once every two years.

The report should include:

- Description of Climate-Related Financial Risks

- Physical risks: impacts from extreme weather, flooding, droughts, heatwaves, wildfires, etc.

- Transition risks: policy changes, carbon pricing, technological shifts, investor pressure, or changing market preferences.

- Assessment of Exposure and Financial Impact

- How these risks could affect revenue, operating costs, supply chains, and asset values.

- Potential financial consequences (e.g., asset impairment, stranded assets, higher insurance or capital costs).

- Governance and Oversight Structures

- How boards and executives oversee climate risks.

- Integration into enterprise risk management (ERM) frameworks.

- Mitigation and Adaptation Measures

- Strategies, targets, or investments to manage identified risks.

- Examples: renewable energy adoption, diversified supply chains, climate resilience planning.

- Reference Frameworks

- Reports must align with TCFD or an equivalent framework recognized by CARB (e.g., ISSB standards).

- Public Disclosure

- The report must be published on the company’s website for public access.

At a Glance: SB 261 Reporting Requirements

| Category | Details |

| Threshold | > USD 500 million global annual revenue |

| Coverage | Any company doing business in California (public or private) |

| Report Type | Climate-Related Financial Risk Report |

| Frequency | Every 2 years |

| Framework Alignment | TCFD or equivalent (ISSB, SEC, etc.) |

| First Due Date | January 1, 2026 (for FY 2025 data) |

| Regulator | California Air Resources Board (CARB) |

| Penalty for Non-Compliance | Up to USD 50,000 per year |

| Assurance Requirement | None currently; subject to future CARB rulemaking |

How SB 261 Changes Climate Risk Disclosure in the U.S.?

- Brings Climate Risk Into the Boardroom

SB 261 formally links climate change to financial risk, requiring board oversight and disclosure of governance. It essentially elevates sustainability from a CSR initiative to a board-level financial concern. - Bridges ESG and Finance Functions

Finance, sustainability, and risk teams must now collaborate to assess how climate hazards or policy changes could affect cash flow, capital expenditure, and insurance costs. - Drives Scenario Analysis and Stress Testing

Companies must model different climate scenarios (e.g., 1.5°C, 2°C, 3°C futures) to understand how revenue and asset values might fluctuate under varying climate pathways. - Increases Transparency to Investors and Regulators

With reports made public, investors can compare companies’ climate resilience and risk management strategies — much like financial performance indicators. - Creates a De Facto National Standard

Because thousands of large U.S. companies “do business in California,” SB 261 effectively sets a national precedent for climate-risk disclosure, even before the SEC finalizes its own rules.

Key Challenges Businesses Will Face

- Integrating Financial and Climate Data

Most companies already track emissions, but few link that data to balance-sheet impacts. Mapping climate events to financial outcomes (e.g., supply disruption → cost of goods sold) will require new data pipelines and analytics tools. - Scenario Modelling and Quantification

Companies are expected to perform TCFD-style scenario analysis; many use NGFS/IPCC inputs to quantify financial impacts. - Governance and Accountability

Boards and CFOs must take ownership. Expect increased scrutiny from investors and regulators on how climate risk is embedded into risk management and capital planning. - Legal and Data Consistency

The challenge lies in aligning disclosures under multiple regimes — SEC climate rules, CSRD (EU), and now California. Inconsistencies can trigger reputational or compliance risks. - Resource and Skill Gaps

Sustainability teams may lack financial modelling experience, while finance teams may lack climate science literacy. Cross-functional collaboration and training will be key.

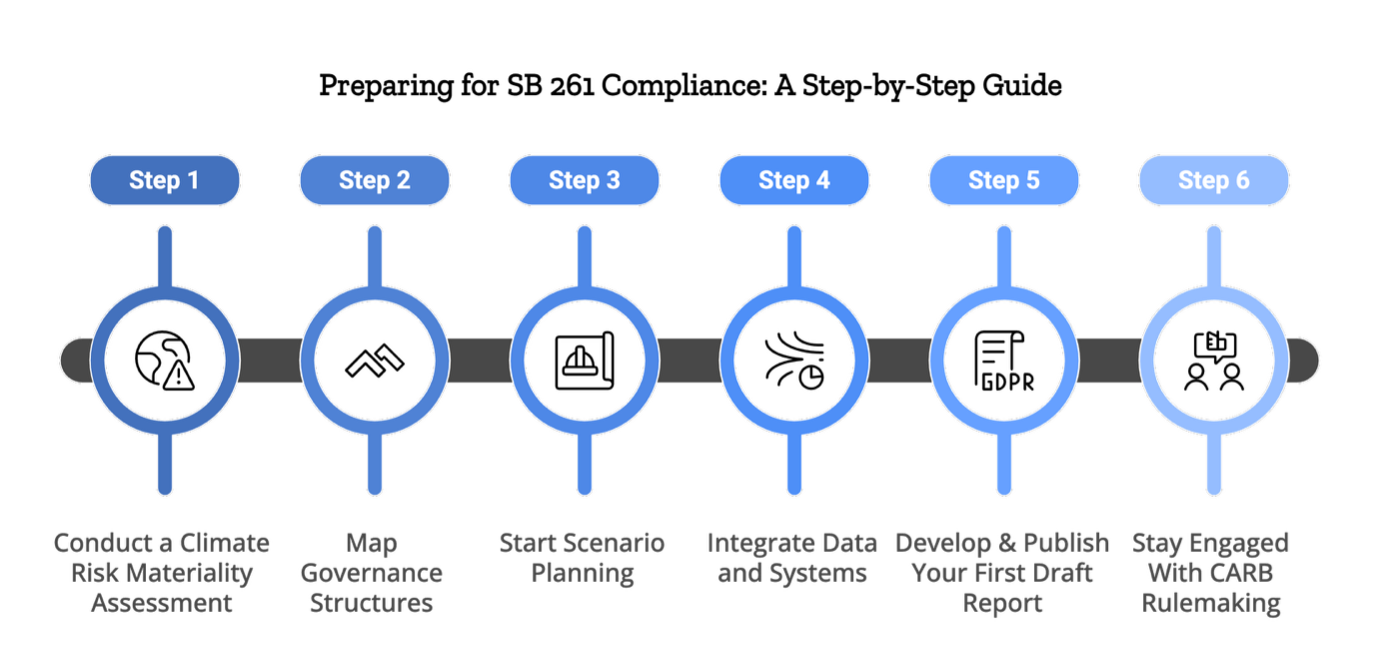

How to Prepare for SB 261 Compliance?

Step 1: Conduct a Climate Risk Materiality Assessment

Identify which physical and transition risks are most relevant to your operations and supply chain.

Step 2: Map Governance Structures

Define board and executive roles for climate oversight. Align with enterprise risk management (ERM) practices.

Step 3: Start Scenario Planning

Use models such as the Network for Greening the Financial System (NGFS) or IEA scenarios to simulate potential financial impacts.

Step 4: Integrate Data and Systems

Centralize climate and financial data in a single system. ESG software like Credibl can automate data ingestion, model exposure, and link climate metrics to financial KPIs.

Step 5: Develop and Publish Your First Draft Report

Even if 2025 data aren’t final, pilot your disclosure in 2024–25. Early action will surface data and process gaps.

Step 6: Stay Engaged With CARB Rulemaking

CARB will issue guidance on reporting templates, assurance, and definitions. Participate in consultations to shape feasible requirements.

Why SB 261 Matters for Investors and Companies Alike?

SB 261’s biggest impact is transparency. Investors will finally see which companies have quantified and planned for climate risks — and which have not.

It also helps level the playing field between sustainability leaders and laggards. Early adopters who disclose robustly may gain reputational benefits, easier access to green finance, and stronger stakeholder trust.

For businesses, SB 261 is a catalyst to embed climate intelligence into financial planning, enhance resilience, and anticipate future regulatory convergence between California, the SEC, and the EU’s CSRD framework.

Conclusion

California’s SB 261 cements the link between climate change and financial stability. By 2026, thousands of companies will be required to publicly explain how rising temperatures, floods, wildfires, or shifts in carbon policy could impact their bottom line.

This is not just compliance; it’s risk foresight. Companies that act now can transform climate disclosure into a strategic advantage — identifying vulnerabilities, reallocating capital, and strengthening investor confidence.

If you’re beginning your climate-risk reporting journey, consider leveraging AI-driven ESG tools like Credibl to automate data collection, align with TCFD, and generate audit-ready financial risk reports in weeks, not months.

Frequently Asked Questions (FAQs)

Q1: When is the first SB 261 report due?

January 1, 2026, covering fiscal year 2025 climate-related financial risks and mitigation strategies.

Q2: Does SB 261 apply to non-California companies?

Yes. Any company “doing business in California” — whether through sales, employees, or operations — that meets the USD 500 million revenue threshold must comply.

Q3: What is considered a “climate-related financial risk”?

Any physical or transition risk that could materially affect revenue, costs, assets, or capital — e.g., wildfires, new carbon taxes, regulatory shifts, or energy-market volatility.

Q4: What frameworks can companies use?

TCFD, ISSB (IFRS S2), or other CARB-approved equivalents. Aligning with TCFD ensures international comparability.

Q5: Is third-party assurance required?

Not initially. CARB may evaluate assurance requirements in future updates, but SB 261 currently focuses on disclosure quality and accessibility.

Q6: What are the penalties for non-compliance?

Civil penalties of up to USD 50,000 per year can be imposed by CARB for failing to publish or update reports.

Q7: How does SB 261 differ from SB 253?

SB 253 covers emissions data (Scopes 1-3); SB 261 covers financial risk exposure and governance. Together, they create a full picture of climate impact and accountability.