Introduction

In sustainability reporting, materiality assessment has emerged as the foundation of credible disclosure. It answers a critical question: Which ESG (Environmental, Social, and Governance) issues really matter to a business and its stakeholders?

From the EU Corporate Sustainability Reporting Directive (CSRD) to GRI Standards, IFRS S1/S2, and India’s BRSR Core, materiality is no longer optional — it is central to compliance, transparency, and strategic decision-making. For exporters, importers, policymakers, and the public, understanding materiality is vital for navigating the future of sustainable trade and governance.

This article explores what materiality assessment is, why it matters, how it works, who it affects, where it applies, its challenges, and what the future holds.

What Is a Materiality Assessment?

A materiality assessment is the structured process of identifying, ranking, and prioritizing sustainability topics most relevant to a company and its stakeholders.

Two primary approaches define today’s ESG materiality landscape:

- Single Materiality: Focuses on how sustainability issues impact a company’s financial performance.

- Double Materiality: Considers both financial impact on the company and the company’s impact on society and the environment.

Under the EU CSRD, double materiality is now mandatory, requiring companies to assess ESG risks both ways. This shift is accelerating global alignment around broader definitions of corporate responsibility.

Why Is Materiality Assessment Important?

- For Companies

Ensures ESG reports focus on relevant issues, avoiding “data overload.” It also helps allocate resources efficiently to address top priorities & strengthens risk management by highlighting long-term ESG exposures.

- For Investors

Provides transparency on financially material risks and opportunities & enables ESG integration into investment strategies and risk-adjusted returns.

- For Policymakers & Regulators

Informs sustainable finance regulations and disclosure mandates & also creates consistency and comparability across industries.

- For the Public & Communities

Demonstrates accountability and builds trust and signals how companies manage their broader impact beyond profits.

According to Deloitte’s 2023 Sustainability Disclosure Study, 89% of investors believe companies should disclose both financially material ESG issues and broader societal impacts — reinforcing the relevance of double materiality.

How Is a Materiality Assessment Conducted?

A robust materiality assessment usually follows five key steps:

Identify Potential ESG Topics

Draw from reporting frameworks (GRI, CSRD, SASB, BRSR).

Benchmark against industry peers and emerging trends (climate risk, biodiversity, AI ethics).

Engage Stakeholders

Consult employees, investors, customers, suppliers, regulators, and communities.

Use surveys, interviews, or AI-driven stakeholder engagement tools.

Assess Significance

Evaluate each issue’s financial impact on the business and societal/environmental impact.

Use quantitative (data analysis) and qualitative (stakeholder sentiment) methods.

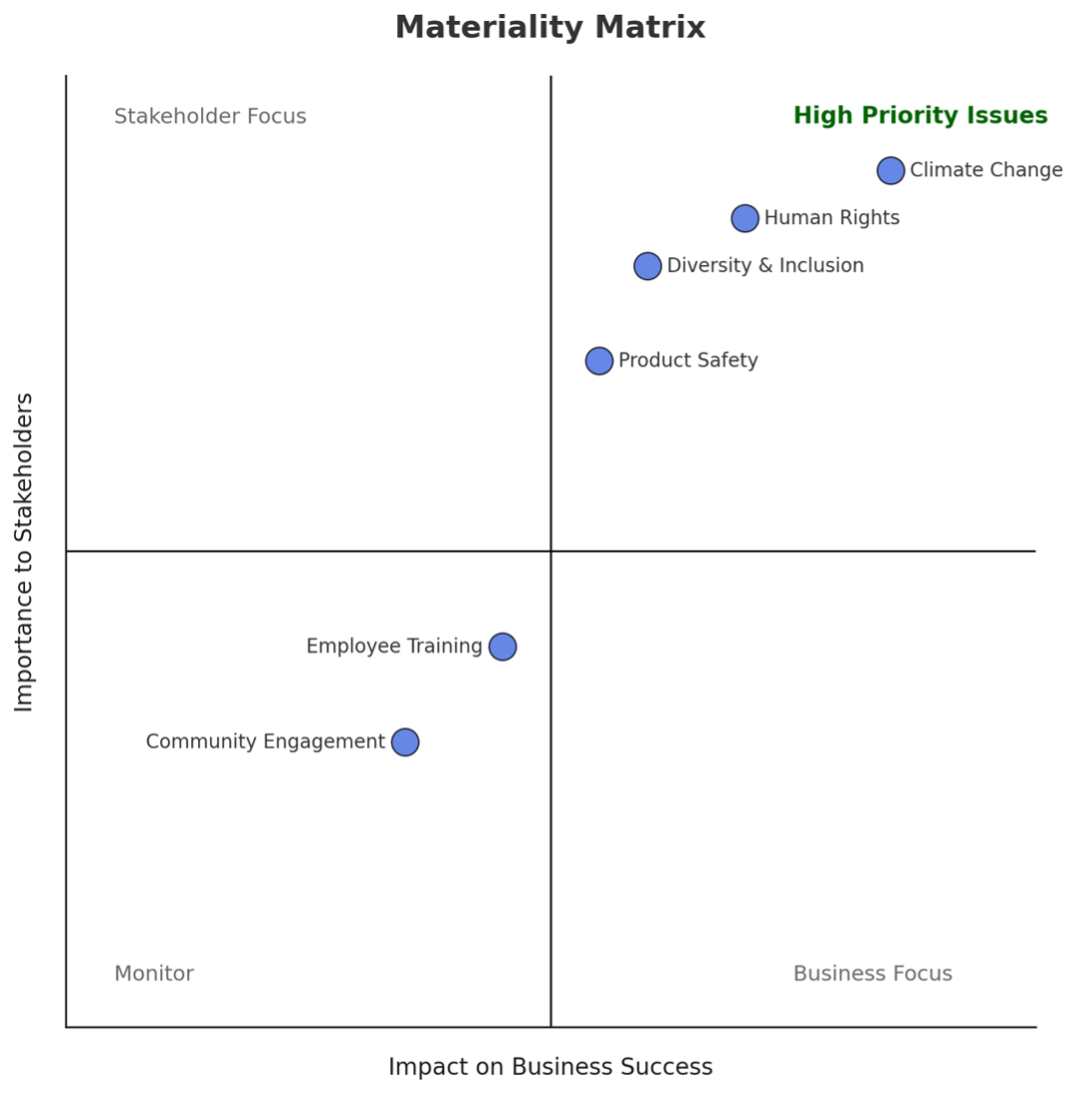

Prioritize & Visualize

Rank issues and plot them on a Materiality Matrix (see graphic below).

Highlight “high-priority” issues that score strongly on both dimensions.

Integrate & Report

Align top issues with corporate strategy, risk frameworks, and sustainability disclosures.

Refresh assessments regularly (every 1–2 years).

Materiality Matrix Graphic

Who Does It Affect?

- Sustainability Teams & Reporting Managers – to design ESG disclosures.

- Exporters & Importers – as ESG compliance becomes a license to operate in global markets (CSRD, CBAM).

- Investors & Banks – to evaluate ESG-related risks before allocating capital.

- Regulators & Policymakers – to set consistent disclosure standards.

- Consumers & Civil Society – who hold companies accountable for their impacts.

Where Does Materiality Apply?

Materiality is now embedded in all major ESG frameworks:

- CSRD (EU): Double materiality required for 50,000+ companies from 2024.

- GRI Standards: Focus on stakeholder-inclusive materiality.

- IFRS S1/S2 (ISSB): Oriented toward financial materiality.

- BRSR Core (India): Mandates disclosure of material ESG topics.

- SEC Climate Rule (US): Requires disclosure of financially material climate risks.

This makes materiality a global requirement that no company can ignore.

Challenges and Best Practices

Challenges

- Stakeholder fatigue from repetitive consultations.

- Inconsistent data across subsidiaries or geographies.

- Dynamic issues: Material ESG topics evolve rapidly (e.g., biodiversity, just transition, AI ethics).

Best Practices

- Refresh assessments every 1–2 years.

- Use digital ESG platforms for data capture, visualization, and audit-readiness.

- Ensure cross-functional participation (finance, legal, sustainability, operations).

- Map to multiple frameworks simultaneously to reduce duplication.

Conclusion

Materiality assessment is not just a compliance exercise. It is a strategic compass that determines how companies focus resources, manage risks, and communicate their true sustainability impact.

By embedding materiality into strategy, businesses can align with global standards, build trust with stakeholders, and future-proof their operations in a sustainability-driven economy.

At Credibl, we help organisations conduct robust, audit-ready materiality assessments. Our AI-powered platform streamlines stakeholder engagement, aligns with CSRD, GRI, and BRSR frameworks, and ensures that materiality processes are transparent, compliant, and future-focused.

Partner with Credibl to make your ESG reporting smarter, faster, and aligned with double materiality.

FAQs

- What is the difference between single and double materiality?

Single materiality looks at how ESG issues affect the company’s financial performance. Double materiality adds the perspective of how the company impacts society and the environment.

- How often should a company conduct a materiality assessment?

Best practice: every 1–2 years, or whenever there are significant changes in regulations, operations, or stakeholder expectations.

- Is a materiality matrix mandatory?

While not always legally required, a materiality matrix is the most widely used tool to visualize and communicate results, and is expected under GRI and CSRD.

- Which regulations require materiality assessments?

EU CSRD, India’s BRSR Core, GRI Standards, ISSB’s IFRS S1/S2, and upcoming SEC rules all require or recommend materiality as a cornerstone of ESG reporting.

- Can technology simplify the process?

Yes. AI-enabled ESG platforms like Credibl automate data collection, stakeholder engagement, and framework alignment, reducing manual effort and ensuring audit-readiness.